Only the strong will survive co-working’s pandemic

The pandemic will fast-track the evolution of the co-working sector, hastening the closure of businesses that fail to maintain the cashflow they need to survive and leaving Australia with just three or four larger operators, according to ASX-listed Victory Office’s boss, Dan Baxter.

The comments come days after the flexible working operator secured $15.3 million in a capital raising to shore up its balance sheet, in order to manage the ongoing impact of COVID-19 and to fund operating costs over the next 12 months following a seven-week voluntary suspension from trading on the ASX.

Mr Baxter told The Australian Financial Review many of the smaller operators – particularly those that limited their offering to co-working space and not serviced office suites – were struggling in the current environment.

“If things continue as they are and slowly improve we will see about three to four players – the stronger and bigger ones – operating in this space,” Mr Baxter said.

“The smaller ones will fall down because it is a capital-intense industry and if the occupancy rate goes down to a very low number they won’t be able to survive, the resilience is not there, which is why you will see the big players, like Regus (now IWG), Victory and Servcorp, there for the long term.”

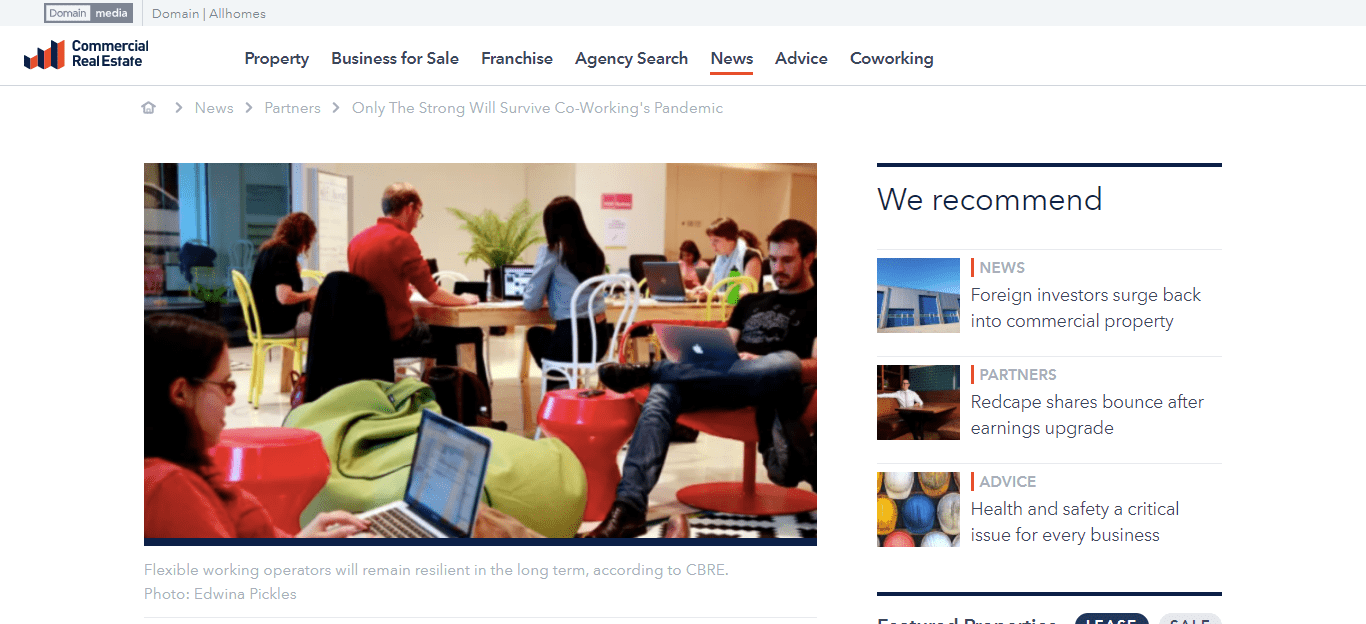

According to a new report by commercial real estate agency CBRE, the closure of flexible working offices across the Asia-Pacific region will be an inevitable consequence of COVID-19 as many operators struggle to survive, but the industry as a whole will remain resilient.

“The flexible space sector faces a number of challenges in the short term, ranging from the decline in new demand to the rapid adoption of remote working,” said CBRE’s global head of advisory and transaction services, Manish Kashyap.

“However, medium- to long-term fundamentals remain sound as corporate occupiers seek out alternative options to reduce costs, reduce capital expenditure and build more flexibility into their real estate portfolios.”

CBRE expects some smaller, unprofitable flexible office operators to fold under the pressure of the pandemic and larger operators on “a relatively solid financial footing to increase their market share at the expense of less established platforms” as part of a broader trend of industry consolidation.

“More merger and acquisition activity among operators is expected,” the authors of the report wrote.

“Closures of unprofitable centres will be unavoidable but surrendered or subleased space is likely to be taken up by other coworking operators that are financially sound, or by tenants seeking fully fitted-out space.”

Flexible working businesses, both co-working and serviced-office operators, are battling to survive through the pandemic. Occupancy levels have plunged in some cases to less than 10 per cent with social distancing forcing people to work from home and many operators temporarily closing facilities or decreasing their operating hours.

Several operators have now put expansion plans on hold and have furloughed or laid off staff to alleviate the rising financial pressure, according to CBRE.

Hub Australia chief executive Brad Krauskopf expects that after COVID-19 some operators will join forces to achieve scale.

“The operators that get through this period, they will have stress-tested the business and there will be a good market for them on the other side of it… I think you’ll certainly get a lot of consolidation where parties join together,” he said.

CBRE says some operators are now pushing to transition to revenue-sharing models with landlords or enter into management agreements.

Others are trying to to negotiate with landlords to obtain subsidies for fit-outs as well as the inclusion of options of long-term lease agreements.

It follows a boom in flexible offices across the Asia-Pacific region with space growing threefold over the past five years, aided by growth in the share economy and a flood of venture capital.

According to CBRE, the rate of growth in flexible office space was already slowing at 20 per cent year-on-year in 2019 as competition among operators intensified and businesses began to re-evaluate their business models.

However, growth slowed even further in the first quarter of 2020 to just 5 per cent year-on-year.

With 71 million square feet across 18 major cities tracked by CBRE, flexible office space equates to 4 per cent of total Asia-Pacific office stock.

CBRE said the most vulnerable cities were those with a higher penetration of flexible space such as Shanghai, Singapore and major office markets in India.